Welcome to our June newsletter, where we’ll dive into residential real estate trends in San Francisco and across the nation. This month, we examine how the money supply is affecting asset price valuations and interest rates.

The increase of money supply started accelerating around 2000 and, since that time, with the exception of the past couple of months, inflation has been extremely low. At the same time, asset prices, like stocks and real estate, have risen considerably. Low inflation suggests that consumers are saving more than they are spending on goods and services. With more money in circulation, interest rates drop. In fact, mortgage rates are hovering near all-time lows, just under 3%.

With low interest rates, more money in circulation, and fewer opportunities to spend money over the last year, homebuyers have flooded the market—and we expect this high housing demand to continue for at least the next 12 months. In addition, most potential buyers are flush with cash and have high credit scores, which has created an incredibly competitive environment and caused housing inventory to drop to historically low levels.

As we navigate this period of high buyer demand and low supply, we remain committed to providing you with the most current market information so you feel supported and informed in your buying and selling decisions. In this month’s newsletter, we cover the following:

- Key Topics and Trends in June: The supply of money in the United States has contributed to increasing asset prices, especially in the housing market.

- June Housing Market Updates for San Francisco: Single-family home prices reached another all-time high, and demand for condos dramatically increased.

Key Topics and Trends in June

The past year saw the highest sales volume and fastest price increases on record, nationally. We want to take a closer look at this massive buyer demand and the ways in which it’s affecting the housing market.

At the start of the pandemic, the housing market looked incredibly unstable: buyers and sellers were pulling out of deals, sales volume and inventory dropped, and unemployment skyrocketed. The uncertainty around the housing market was short-lived, however, and it became clear that homes were going to have a remarkable year.

The sheer number of highly qualified buyers who were entering the market seemed to come out of nowhere, and we were left wondering where all this money had been hiding before the pandemic. As we dug into the data, we saw that the money was out there, but people were simply not spending it.

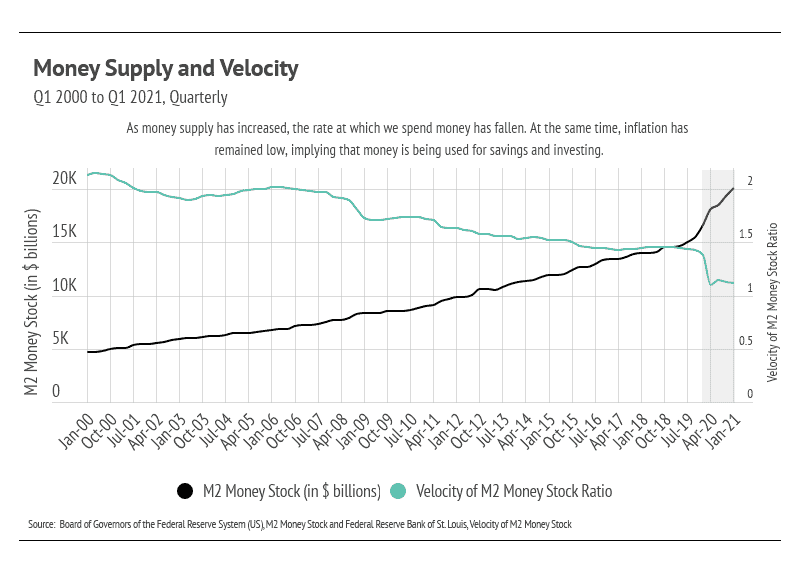

The graph below shows the money supply (M2) in the United States and the velocity of money, which measures how much consumers and businesses are spending (higher velocity equates to more spending, and vice versa). When the money supply and velocity increase, we tend to see inflationary periods. As you can see from the chart, however, the money supply increased dramatically (3x) over the last 20 years, while velocity decreased. In other words, more money has not driven the equivalent production of more goods and services, implying that consumers are saving and/or investing. Over the last year, the money supply has increased even more because of COVID-19 relief and the Federal Reserve’s monetary policies, putting even more money in consumers’ pockets.

Using the S&P 500 and the housing market as examples, we can see the effect that the money supply has had, especially over the last year. The S&P 500 increased around 54% from March 2020 to March 2021, and the Case-Shiller 20-City Home Price Index, which measures the aggregate home prices in the 20 largest metro areas, rose 14%. Stock prices benefit considerably from increased money supply due to their liquidity and fungibility. Home prices rose substantially, especially considering their illiquid nature. Notably, we aren’t seeing a transfer of money out of stocks and into housing; rather, we’re seeing cash going into both asset classes, which means that there is a large amount of money in circulation.

An increase in money supply also tends to lower interest rates. As shown in the chart below, mortgage rates have definitely declined over the last 20 years, and we’re currently hovering at historically low rates, which increases housing affordability despite the rising prices.

We don’t expect the same level of buying in 2021 that we saw in 2020, mostly because of the home undersupply issue. The environment, therefore, is right for demand to outpace supply in 2021. We’ve reached near-perfect conditions for buyers—high credit scores, large down payments, and low-rate financing—so we anticipate a competitive landscape for buyers throughout the year.

While the market remains competitive for buyers, conditions are making it an exceptional time for homeowners to sell. Low inventory means sellers will receive multiple offers with fewer concessions. Because sellers are often selling one home and buying another, it’s essential that sellers work with the right agent to ensure the transition goes smoothly.

June Housing Market Updates for San Francisco

During May 2021 in San Francisco, the median single-family home price rose to another all-time high, and condo prices edged higher. Year-over-year, single-family home prices meaningfully increased, up 20%, while condo prices rose 18%.

In 2020, single-family home inventory increased to its highest level since 2011. From May to September 2020 (five months), inventory exploded. But we need to look at it through the lens of a city in a constant state of single-family home undersupply. Despite such a meteoric rise, inventory fell even faster than it rose, which speaks to the desirability of San Francisco. By January 2021, inventory declined to lower levels than January 2020, then ticked up slightly in February and March before going lower still in April and May 2021. As you can see from the chart, sales outpaced new listings in April and May. With such a consistently high level of demand, prices will likely continue to appreciate throughout 2021.

The number of condos on the market fell in May to a lower level than last year. Demand for condos has come back strong, and sales outpaced new listings in April and May. Sales in May 2021 significantly outpaced sales in both May 2020 and 2019.

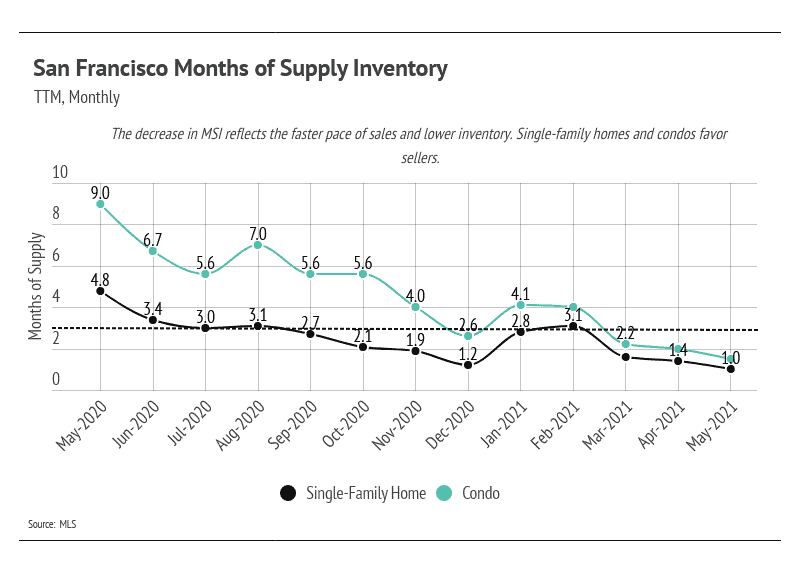

Both single-family homes and condos spent less time on the market in May 2021 than they did in May of last year. As we’ll see, the pace of sales has contributed to the low Months of Supply Inventory (MSI) over the past several months.

We can use MSI as a metric to judge whether the market favors buyers or sellers. The average MSI is three months in California (far lower than the national average of six months), which indicates a balanced market. An MSI lower than three means that there are more buyers than sellers on the market (meaning it’s a sellers’ market), while a higher MSI means there are more sellers than buyers (meaning it’s a buyers’ market). In May 2021, the MSI dropped to one month of supply for single-family homes and 1.5 months for condos, indicating that the market strongly favors sellers.

In summary, the high demand and low supply present in San Francisco have driven home prices up. Inventory will likely remain low this year with the sustained high demand in the area, potentially lifting prices higher. Overall, the housing market has shown its value through the pandemic and remains one of the most valuable asset classes. The data show that housing has remained consistently strong throughout this period.

We expect that the number of new listings will increase in the summer months.The current market conditions can withstand a high number of new listings coming to market, and more sellers may enter the market to capitalize on the high buyer demand. As we navigate the spring season, we expect the high demand to continue, and new houses on the market to be sold quickly.

As always, we remain committed to helping our clients achieve their current and future real estate goals. Our team of experienced professionals are happy to discuss the information we have shared in this newsletter. We welcome you to contact us with any questions about the current market or to request an evaluation of your home or condo.